The UK will return to growth this year, but that growth will not be strong enough to spare the Labor government another tax hike before the next election, according to an annual survey of economists by the Financial Times.

A survey of 96 leading economists found that while the UK is likely to overtake France and Germany in 2025, previously announced tax increases for businesses and individuals could undermine jobs and beyond economy.

Most economists expected only a mild rate of expansion this year, less than the 2 percent recovery projected by the Office for Budget Responsibility in 2025.

“Growth will exceed government and OBR forecasts,” said Maxime Darmet, senior economist at Allianz Trade. “Therefore, tax revenues will probably be lower.”

All but a few respondents said the British chancellor Rachel Reeves she would raise taxes again before the next general election, expected in 2029, despite her protests that Britain will not have another budget with big tax increases this parliament.

Andrew Oswald, professor of economics and behavioral sciences at the University of Warwick, said there would be a “dawning… . . that without an increase in income tax and VAT, we cannot achieve the damn sums”.

Reeves, who took office warning that Labor had inherited “the worst circumstances since the Second World War”, increased employers’ National Insurance contributions by £25bn in her Autumn Budget – a move due to come into effect in April.

“The government decided to scare business, which hit confidence,” said Sir Howard Davies, professor of practice at the Paris Institute of Political Science (Sciences Po) and former director of the London School of Economics.

He added that given the impact on confidence, the UK would remain “just outside the Champions League” in the G7 growth rankings.

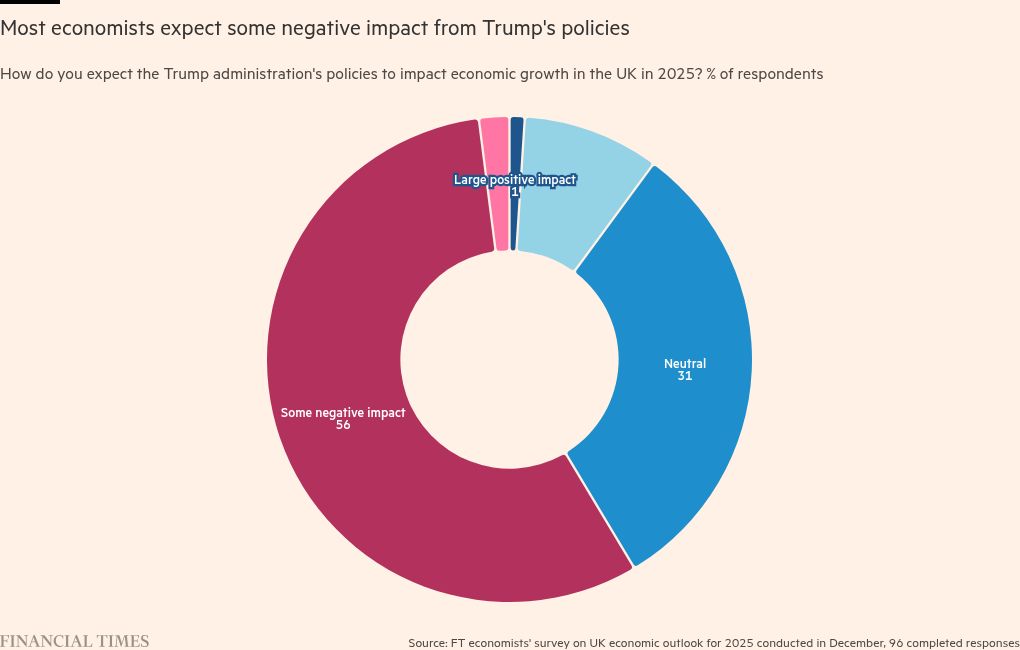

Britain’s greater political stability and services-based economy meant it would fare better in 2025 than France and Germany, which could be hit harder by potential US tariffs threatened by President-elect Donald Trump, the survey found. However, most economists expected a certain negative effect of Trump’s policies on the UK.

Economists said UK growth would continue to lag the US as the temporary stimulus from higher government spending outlined in the Budget faded and higher labor costs hit employers.

Wages will continue to rise in real terms, which will make people feel a little better, many economists said. However, they added that any improvement in sentiment will be limited as prices and borrowing costs are still high and the growing tax burden is fueling concerns about job security.

Fhaheen Khan, senior economist at manufacturing trade group Make UK, said the increase in employers’ National Insurance contributions would be a “tough pill to swallow” for industries whose costs have been rising for years.

Stubborn inflation would also limit the Bank of England’s ability to cut interest rates, and the UK would continue to suffer from chronically weak investment and productivity, the research found.

The FT investigation was closed before a series of published data showed the scale of the challenge facing Reeves this year.

Growth started to reverse at the end of 2024, s GDP in stagnation during the third quarter and contracting in October. At the same time, price pressures persisted and business sentiment worsened.

Most economists believe that the return to growth will be supported by an initial increase in government spending and by consumers becoming more willing to spend their accumulated savings.

But forecasts compiled by Consensus Economics in December, ahead of the latest figures, showed the average forecast among economists was for GDP growth of just 1.3 per cent in 2025. Most respondents to the FT poll had similar expectations.

Andrew Goodwin, chief UK economist at consultancy Oxford Economics, said the OBR was “overly optimistic about the potential for the public sector to drive growth” when it hit its 2 per cent GDP growth forecast for 2025.

Diane Coyle, a professor of public policy at the University of Cambridge, added that returning the economy to the growth rate it was at before the 2008 financial crisis “would require much more investment in public services and infrastructure than it has [Reeves] is the budget for”.

Other respondents described Labour’s current plans, which imply that growth in spending on public services will slow sharply from 2026, as “fabulous”, “unrealistically tight” and “politically implausible”.

Closing the gap with additional public borrowing would be difficult, argued Paul Dales of consultancy Capital Economics, who said the UK was “close to the limit” of what financial markets would tolerate.

The chancellor may decide to wait until later in parliament to raise taxes, given the political cost of such a quick turnaround.

Ray Barrell, professor emeritus at Brunel University, said any changes in 2025 were likely to be “subtle”, such as reforms to property taxation or duties on tobacco and alcohol.

Ricardo Reis, professor of economics at the LSE, said that because the money was earmarked for investment projects that had not yet been announced, “they can always be canceled or postponed if there is a crisis”.

But some respondents said Reeves may decide to make unpopular changes sooner rather than later.

“Most chancellors go through the pain in parliament early on,” observed Jonathan Haskel, a professor at Imperial College London and a former member of the Bank of England’s Monetary Policy Committee.

Slow growth isn’t the only reason government spending plans will come under pressure in 2025.

Most respondents to the survey said they also expect inflation to remain above the BoE’s target throughout the year, so the central bank will take only “small steps” to cut interest rates – which would keep the cost of servicing the government higher than in previous years.

Most economists did not see slightly above inflation as a big problem for the economy. The bigger problem, according to Bart van Ark, director of the University of Manchester’s productivity institute, is that “price levels are still perceived as high, even after real wage corrections”.

Nick Bosanquet, a former professor at Imperial College now at consultancy Aiming for Health Success, said the “anxiety” about inflation meant “most households will be solvent . . . but with a lot of worries about the future”.

Bronwyn Curtis, chairman of TwentyFour Income Fund, added: “A major positive effect [of strong wage growth] is in the past, and taxation of the working population. . . it won’t make them feel better.”

Higher taxes should eventually lead to better public services that will make households feel more secure, even if they are less able to spend, said Kate Barker, a former member of the BoE’s monetary policy committee.

Simon Wells and Liz Martins, economists at HSBC, said the labor market was the “biggest unknown” for 2025, pointing to corporate plans to deal with the coming rise in employment costs through downsizing, automation, offshoring, wages or by increasing the price.

“It’s all negative for British workers,” they added. “So the question is how the pain will spread.”

Additional reporting by Jim Pickard